Overview

This vignette introduces highest probability density (HPD) summaries in koma. Two related summaries are provided:

-

hdr()computes highest density regions (HDRs) using a kernel density estimate, following Hyndman (1996). For multimodal draws, HDRs can have multiple disjoint intervals. (Hyndman 1996) -

hdi()computes highest density intervals (HDIs), defined as the shortest interval containing a target probability mass. HDIs are always a single interval.

Use HDRs when you want multimodal structure to be preserved. Use HDIs

when you want a single concise interval. For full function details, see

?hdr and ?hdi.

Draws-based HPD summaries

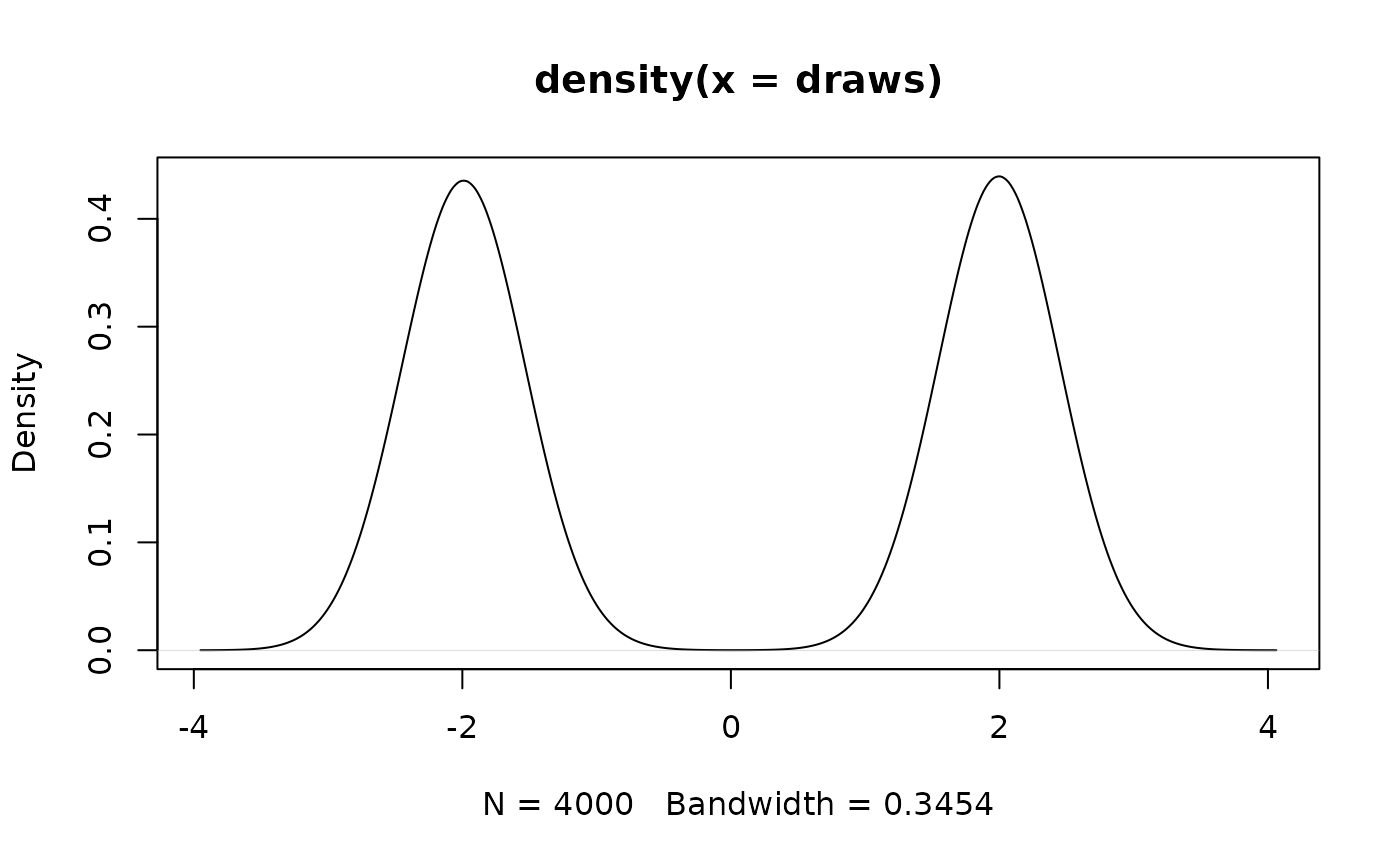

We start from a synthetic bimodal sample to highlight the difference.

set.seed(123)

draws <- c(

rnorm(2000, mean = -2, sd = 0.3),

rnorm(2000, mean = 2, sd = 0.3)

)

plot(stats::density(draws))

hdr_res <- hdr(

draws,

probs = c(0.5, 0.99),

integration = "grid"

)

hdi_res <- hdi(

draws,

probs = c(0.5, 0.99)

)

hdr_res$intervals$level_99

#> lower upper

#> [1,] -3.1657900 -0.8137866

#> [2,] 0.8240061 3.1642691

hdi_res$intervals$level_99

#> lower upper

#> [1,] -2.675314 2.646959In this example, the 99% HDR will typically return two intervals, one around each mode, while the 99% HDI returns a single interval that spans both modes.

Tuning HDR estimation

HDRs are based on a kernel density estimate, so you can adjust bandwidth, kernel choice, or the integration strategy:

hdr_tuned <- hdr(

draws,

probs = 0.9,

bw = "nrd0",

adjust = 1.2,

kernel = "gaussian",

integration = "monte_carlo",

mc_use_observed = TRUE,

mc_quantile_type = 7

)HDR and HDI from model estimates

If you have a koma_estimate, you can compute HPD

summaries over coefficient and variance draws. The helpers return nested

lists indexed by variable, parameter block, coefficient name, and

probability level.

# Define a small system

equations <- "y ~ x + y.L(1)"

exogenous_variables <- "x"

sys_eq <- system_of_equations(

equations = equations,

exogenous_variables = exogenous_variables

)

# Simulate data (small sample for speed)

gamma_matrix <- matrix(1, nrow = 1)

beta_matrix <- matrix(c(0.2, 0.5, 0.3), nrow = 3)

sigma_matrix <- matrix(0.01, nrow = 1)

sample <- generate_sample_data(

sample_size = 80,

sample_start = c(2000, 1),

burnin = 20,

gamma_matrix = gamma_matrix,

beta_matrix = beta_matrix,

sigma_matrix = sigma_matrix,

endogenous_variables = "y",

exogenous_variables = "x",

predetermined_variables = "y.L(1)"

)

ts_data <- lapply(sample$ts_data, function(x) {

as_ets(x, series_type = "rate", method = "diff_log")

})

# Estimate with fewer draws for a quick example

dates <- list(

estimation = list(start = c(2000, 3), end = c(2019, 4))

)

estimates <- estimate(

ts_data,

sys_eq,

dates,

options = list(gibbs = list(ndraws = 400, burnin_ratio = 0.5, nstore = 1))

)

# HDRs from coefficient draws

hdr_est <- hdr(estimates, probs = c(0.5, 0.99))

summary(hdr_est)

# HDIs from coefficient draws

hdi_est <- hdi(estimates, probs = c(0.5, 0.99))

summary(hdi_est)

# Example: inspect the 99% beta interval for x in equation y

hdi_est$intervals$y$beta$x$level_99You can also visualize HDR results directly:

plot(hdr_est)For more complete estimation and forecasting examples, see the getting started vignette.